Debt Funds in India: Meaning, Types, Benefits, and How to Invest

Debt Funds in India: Meaning, Types, Benefits, and How to Invest

These are debt funds.

If you have ever wondered where to park money for 6 months, how to earn relatively better returns without taking equity risk, or how to build stable layer of your portfolio this guide is for you.

What Are Debt Funds?

Debt mutual funds are funds that invest primarily in fixed-income instruments — government securities, corporate bonds, treasury bills, commercial paper, certificates of deposit, and other money market instruments.

When you invest in a debt fund, the fund lends money to governments or companies in exchange for regular interest payments and the return of principal at maturity. The fund pools your money with other investors' money and builds a portfolio of such instruments.

Unlike equity funds, debt funds do not own a stake in companies. They are lenders, not owners. This makes them structurally more stable, though not entirely without risk.

How Do Debt Funds Generate Returns?

Debt funds earn returns in two ways:

Interest income (accrual): The bonds and securities in the portfolio pay periodic interest. This accrues in the fund's NAV daily.

Capital appreciation (or depreciation): Bond prices move inversely to interest rates. When interest rates fall, existing bond prices rise and vice versa. Funds that hold longer-duration bonds experience more price movement.

Understanding this relationship is essential. A debt fund is not a traditional savings instrument. Its NAV fluctuates, sometimes significantly based on interest rate movements, credit events, and market liquidity.

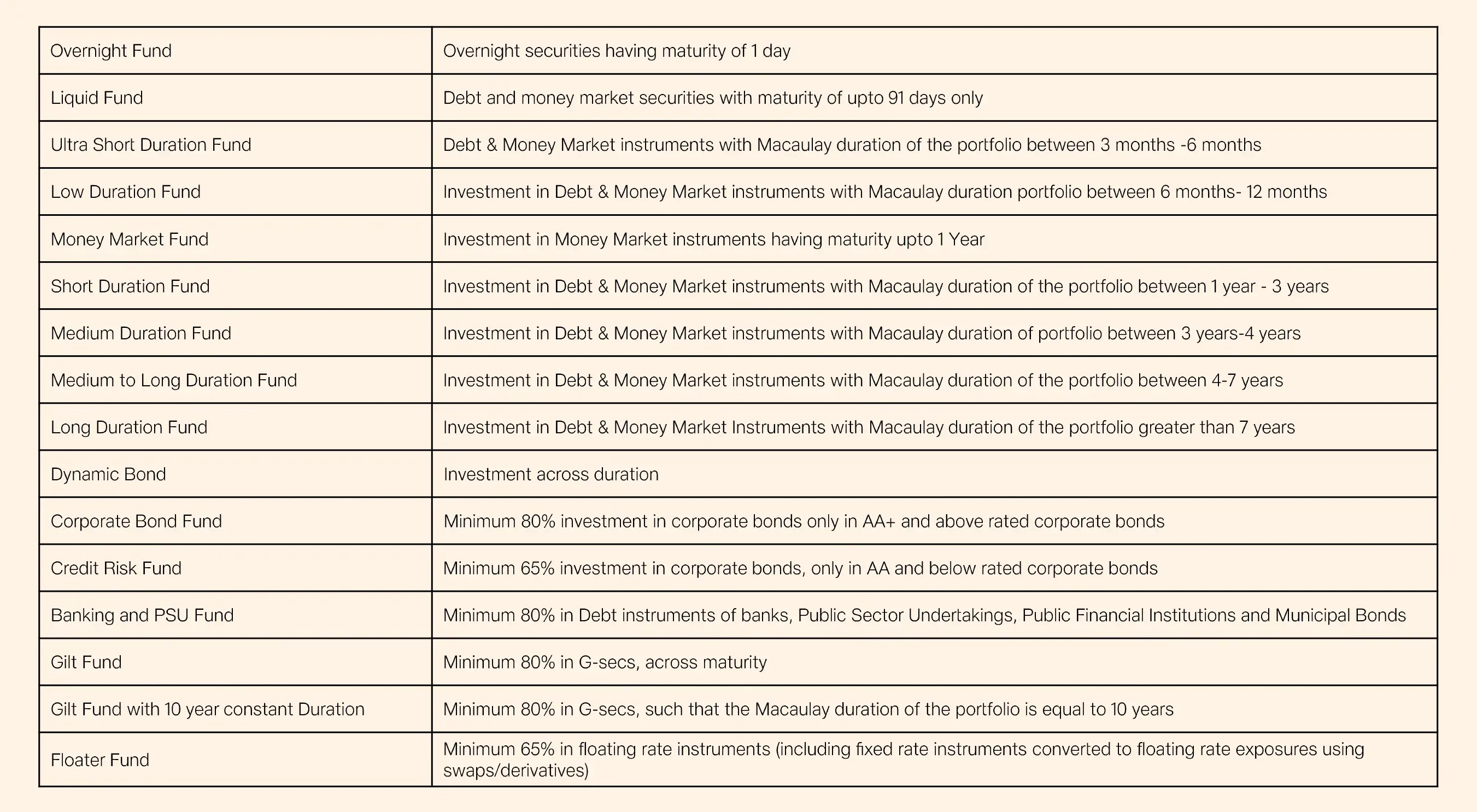

Types of Debt Funds in India SEBI has categorised debt mutual funds into 16 distinct categories. Here are the most important ones:

Source:AMFI

Tax Treatment of Debt Funds

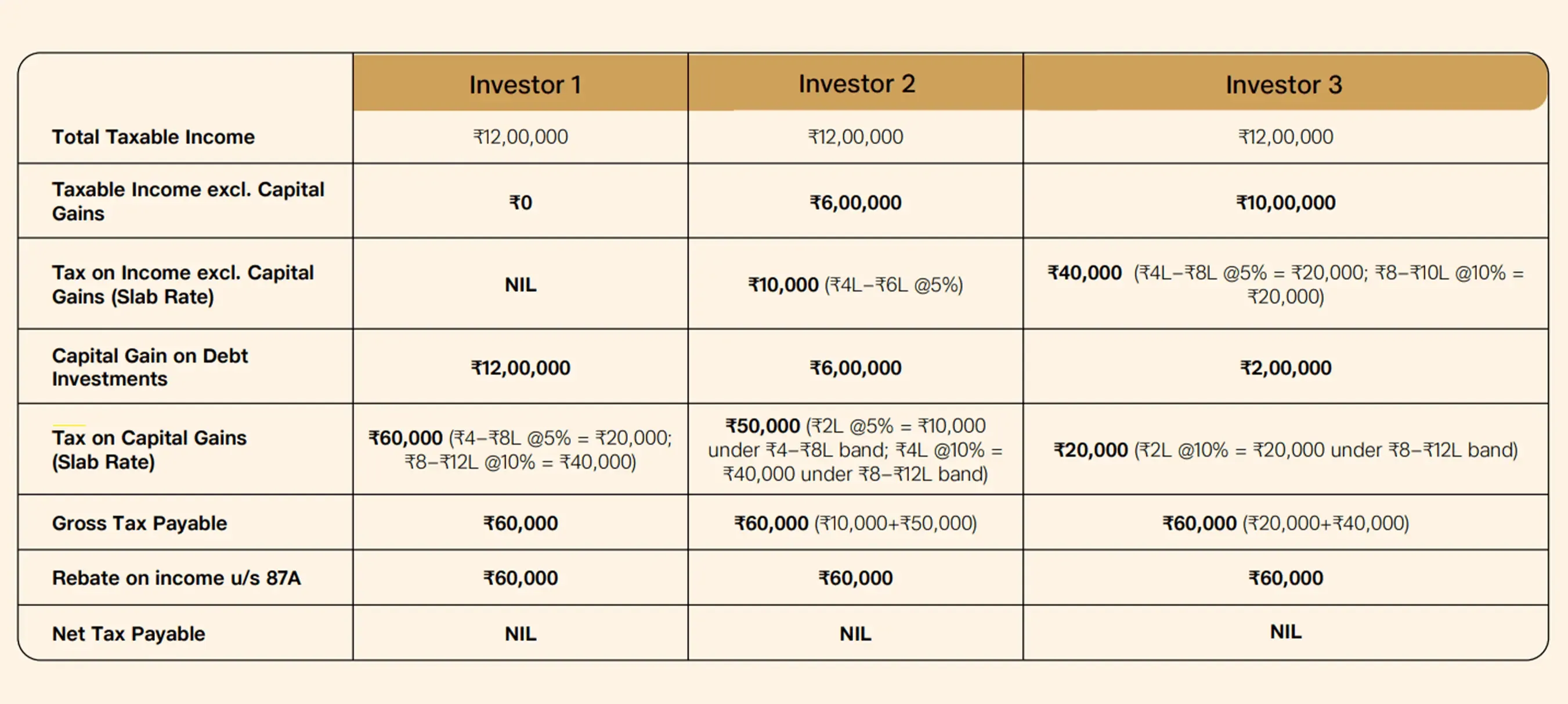

The Finance Act, 2025 revisions in taxation have notably enhanced the appeal of debt mutual funds for investors with annual taxable income of up to ₹12 lakh*

Tax treatment of gains from debt mutual funds is subject to applicable law and individual circumstances. Taxpayers with total taxable income up to ₹12,00,000, net tax liability on such gains may be nil after applying the rebate under Section 87A (Income Tax Act), where conditions are met

Taxation benefit under new tax regime for individuals

As per the Income tax Act, under new tax regime, any individual with a taxable income upto INR 12 lakh will have zero tax liability

Illustration Source: Internal. Cess and surcharge not considered while calculating tax. Investors are advised to consult their tax advisor. Rebate u/s 87A is as per Income Tax Act

Who Should Invest in Debt Funds? Debt funds serve a range of investor needs:

Conservative investors who prefer more stability and regular income without equity volatility.

Investors with short to medium-term goals — a holiday in 1 year, a car purchase in 2 years, a home down payment in 3 years — where high equity exposure may not be suitable

High-income earners who want to defer tax liability to a future year when their income may be lower.

Investors building the stable layer of a balanced portfolio, complementing equity exposure with a debt cushion.

Corporates and HNIs managing treasury or surplus funds seeking alternatives to traditional savings accounts.

Risks in Debt Funds You Should Know Debt funds are not risk-free. The two primary risks are:

Interest Rate Risk When RBI raises interest rates, bond prices fall — and so does the NAV of debt funds holding those bonds. Longer-duration funds are more exposed to this risk.

Credit Risk If the issuer of a bond in the fund's portfolio defaults or gets downgraded, the fund's NAV can fall sharply. This is why fund selection matters in debt investing — the fund's credit quality profile is as important as its returns history.

Credit risk funds, by design, take on higher credit risk for higher yield. For most retail investors, sticking to high-quality funds (corporate bond, banking and PSU, gilt, liquid) may be more appropriate.

How to Choose the Right Debt Fund

Match duration to your investment horizon. One of the most important considerations in debt fund selection - If you are investing for 3 months, a liquid fund could be appropriate. For 2 years, a short duration fund is often considered. Mismatching duration to horizon is among the most common mistakes in debt fund investing.

Check the portfolio's credit quality. Look at the percentage of AAA and sovereign-rated securities in the portfolio. Higher credit quality generally corresponds to lower credit risk.Avoid chasing past returns. A debt fund that generated unusually high returns in a particular year by taking duration or credit exposure may not align with your objectives, as the same risks can reverse quickly under changing market conditions.

A Simple Framework for Using Debt Funds

Here is a practical framework to think about where debt funds fit in your financial life:

Emergency fund → Liquid fund or overnight fund. High liquidity, lower interest rate sensitivity.

Short-term goals (6 months–2 years) → Ultra short, low duration, or short duration funds.

Medium-term goals (2–4 years) → Short or medium duration funds or banking and PSU funds are often considered

Interest rate view play → Dynamic bond funds or gilt funds for investors who may have understanding of the rate cycle and can handle volatility.

Conservative long-term allocation → Corporate bond funds or banking and PSU funds may provide a stable layer of a core long-term portfolio.

Final Thought: Debt Funds Are Not Boring — They Are Necessary

A well-chosen debt fund could help align with your short term goals, , provide the ballast when equity markets correct, and ensures that your money is always working

The right debt fund, in the right bucket, for the right duration — this isn’t routine investing. It’s thoughtful capital allocation.