Tapping into India's transformation

Tapping into India's transformation

Issued by BlackRock Investment Institute

India’s GDP is projected to grow at 6.5% in 2025, well above global and emerging market averages, according to the IMF. We expect structural drivers like demographics and rising productivity to support India’s long-term economic outperformance.

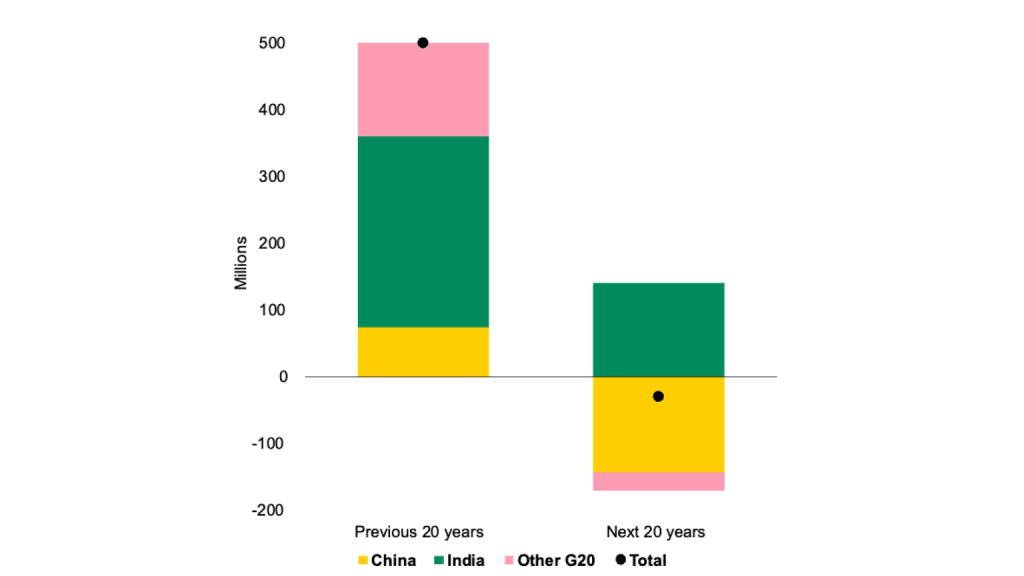

India’s working-age population is set to grow by over 140 million in the next 20 years, while many major economies face declines, according to the United Nations population projections. This demographic dividend provides a foundation for sustained growth, setting India apart globally. Yet unlocking this potential will likely depend on higher female workforce participation and policies that boost skills and job creation, in our view.

We are launching Indian rupee-denominated capital market assumptions (CMAs) to help strategic asset allocations better capture India’s long-term potential, reflecting our view that Indian assets deserve a larger role in global, long-term portfolios.

Bucking the trend

Change in working-age populations, past vs. forecast.

Forward-looking estimates may not come to pass. Source: BlackRock Investment Institute, United Nations, with data from Haver, March 2024. Notes: The chart shows the past change in working-age population (15-64 years old). and the UN’s forecast change over the next 20 years.

India’s structural strengths, in our view, outweigh near-term softness from weak sentiment and U.S. trade uncertainty. Focusing too narrowly on cyclical trends — like slower near-term growth — risks missing the broader structural story and the opportunities it presents, in our view

Recent signs of moderating growth and easing inflation have prompted the Reserve Bank of India to cut interest rates, with further cuts expected to steepen the yield curve. We see Indian government bonds as having attractive income potential, given the higher yields on offer relative to several global peers. Their upcoming inclusion in the JPMorgan GBI-EM index is poised to increase foreign demand, we believe, further supporting this asset class within diversified portfolios.

The MSCI India equity index has lagged broad developed and emerging market indexes since hitting a record high in September 2024, weighed down by slowing growth, valuation concerns and uncertainty over U.S. policy. MSCI India trades at 21.5 times forward earnings, above historical averages, according to LSEG data. We believe robust corporate earnings and lower interest rates can sustain current valuations. India’s exports to the U.S. account for less than 5% of its GDP, limiting its exposure to potential U.S. tariffs compared to more vulnerable economies.

With strong structural drivers in place in our view, we see an opportunity for global investors to increase allocations to large-cap Indian equities directly — rather than through broad indices — to above-benchmark levels.

Download PDF Report

Meet the author

Nicholas Fawcett

Senior Economist, BlackRock Investment Insitute

Vivek Paul

Global Head of Portfolio Research, BlackRock Investment Institute

Ben Powell

Chief APAC and Middle Investment Strategist, BlackRock Investment Institute

Lora Qian

Portfolio Strategist, BlackRock Investment Institute

Disclaimer

The information contained in this article is for general purposes only and not an investment advice in any manner. Investors should seek professional advice before taking any investment-related decisions.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

SIP does not assure a profit or guarantee protection against loss in a declining market. The information herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the investors. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. The Sponsor, the Investment Manager, the Trustee or any of their directors, employees, affiliates or representatives (“entities & their affiliates”) do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information. Investors are suggested to rely on their own analysis, interpretations & investigations. Investors are also suggested to seek independent professional advice in order to arrive at an informed investment decision. Entities & their affiliates including persons involved in the preparation or issuance of this article shall not be liable in any way for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including on account of lost profits arising from the information contained in this article. Investor alone shall be fully responsible for any decision taken on the basis of this article.

Source